State Farm Insurance Company

Click for PDF version of George Mecherle -- State Farm Insurance Company

-- Biography

Click for George Mecherle - Wikipedia page

Introduction

George Mecherle

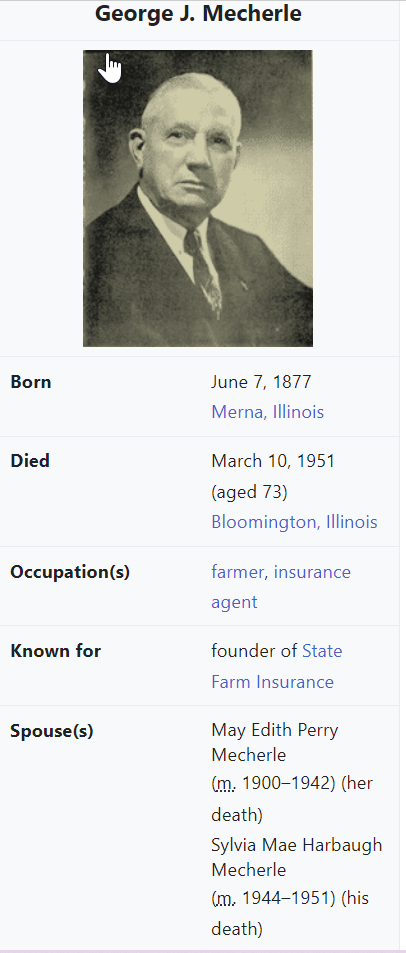

Picture of George Mecherle and Life Stats -- State Farm Insurance Company

Picture of George Mecherle and Life Stats -- State Farm Insurance Company

October 25, 2014

GEORGE MECHERLE

STATE FARM INSURANCE COMPANY

George Mecherle was the founder of the State Farm Insurance Companies. One of his motivations for establishing the company was an ethical impulse to right a perceived wrong too high a price being charged to local farmers for automobile insurance. That ethical consumer orientation subsequently guided the companys growth and change, making Mecherle a notable case study of business ethics.

Mecherle was born on June 7, 1877 on a farm nine miles outside of Bloomington, Illinois.

For the first 18 years of his adult life he was a highly successful farmer. He initially rented the land which he farmed but eventually saved enough to buy his own property. By the age of forty he owned 480 acres of prime Illinois farm land along with a collection of the most modern farm machinery available. He also owned a prized herd of shorthorn cattle and Poland China hogs.

Mecherle might have remained a farmer for his entire working life were it not for the fact that his wife, Mae, had developed a serious arthritis problem. Doctors recommended that she move to a warm southern climate. So,at the age of 40, Mecherle quit farming and moved to Florida. The change of climate did not seem to help Mae Mecherle. So the couple returned to Bloomington, Illinois. There they lived off the rental income from their farm land.

The Mecherles had a comfortable standard of living in Bloomington and their retiree lifestyle was considered normal for that era. But Mecherle soon became bored. Work was what he needed in order to feel fulfilled. And so he took a job as a salesman for an automobile insurance company. That job opened his eyes to the possibilities of developing new, low cost insurance policies that would benefit the consumer and still generate a satisfactory profit. His ideas were not warmly received by his employer and a discouraged George Mecherle left to take a new job selling tractors.

Mecherle was a successful tractor salesman. But he could not stop thinking about his novel automobile insurance concepts. And so, in spite of warnings by friends, he eventually decided to resign from his tractor sales job and devote all of his time and energy to establishing a company to sell automobile insurance.

The concept which Mecherle had in mind was that of a company based on mutual principles. The company would sell automobile insurance to farmers throughout the state of Illinois. Mecherle believed that this form of organization and this method of restricting policy holders to a low risk group of customers would significantly lower the cost of providing the insurance. And the farm customers would thereby be able to purchase insurance for a price significantly lower than anything else then available.

Mecherle planned to get operating costs even lower by as agents persons who were already selling mutual farm fire insurance. Such individuals could easily add automobile insurance as a member service and Mecherle could avoid the cost of establishing a full time sales force of his own.

Mecherle expected to reduce operating costs even more by centralizing a number of functions usually performed by agents. Billing and collecting were two of the functions he had in mind. In addition, he planned to reduce risks by requiring policies to be renewed every six months. That policy would allow the company to adjust rates in the light of the previous six months experience.

These ideas were not entirely original with George Mecherle. He had seen the basic concept being practiced by the nearby Tazewell County Farm Bureau. But Mecherle had the vision to see how the concept could be expanded and improved.

Mecherle also had the courage to pursue the concept in spite of widespread criticism of his ideas. Friends pointed to a Bloomington insurance company that had recently gone bankrupt and warned George that he could suffer the same fate. And when Mecherle traveled to Chicago to present his plan to Herman Ekern, known as the best insurance lawyer in Illinois, Ekern pointed out flaws in the plan and tried to discourage Mecherle from proceeding.

But George persisted. With the help of another attorney, Erwin Meyer, Mecherle eventually worked out a detailed operational plan whereby members of the Illinois State Association of Mutual Insurance Companies would invest in a new company to be called the State Mutual Automobile Insurance Company. The new State Farm company would then contract with Mecherle to be its general agent.

On March 29,1922 the new company was incorporated and George Mecherle took to the country roads in search of clients. By the end of May Mecherle and four fellow salesmen had obtained more than 400 applications for the companys automobile insurance. That was twice the number required by the State of Illinois for issuance of a license to sell insurance. So, on June 8, 1922, the day after George Mecherles forty-fifth birthday, the company held its organizational meeting.

Under George Mecherles direction the new insurance company grew rapidly. By 1924 there were over 3,800 policy holders; by 1931 there were more than 369,000.

Some of that growth was due to the fact that Mecherle had put together a program which offered the customer an unusually low cost. Another cause was the fact that Mecherle emphasized superior customer service. A third factor was Mecherles ability to attract talented home office and field personnel. The people he hired tended to be inspired by Mecherles vision of the company as a servant of the customer. They were also energized by the trust, freedom of action and loyalty they received from Mecherle.

Mecherles original business vision was limited low cost automobile insurance for Illinois farmers. But he quickly developed a desire to spread his low cost service to a wider group of customers. In addition, as State Farm improved its knowledge of the insurance market place, Mecherle came to belief that there were opportunities to offer lower prices and better services in other lines of insurance. And so, over the objections of many of the members of his board of directors, Mecherle expanded the automobile insurance business to cover city dwellers in addition to farmers. Next, with some directors still expressing misgivings, he expanded the company into other states. Then the company began offering life insurance (1929). And in 1935 State Farm began to offer fire insurance.

George Mecherles leadership was a prominent feature of State Farms expansion. As one biographer put it, George Mecherle (was) the dominant figure in all the affairs of the State Farm companies

In

(the) early days

State Farm

had been very nearly a one man operation. His magnificent presence and dynamic personality

towered over all who came to work for him. And even when the company had grown to the tremendous size it was in the last years of his life, this same personality and presence continued to shine over the entire organization ( Schriftgiesser, pp.227-228 ).

From his associates on every level (Mecherle) demanded three things: willingness to work hard, faith in the organization, (and) loyalty to the spirit of State Farm

In return he gave his associates what he demand from them. He was no swivel-chair commander, but the hardest worker of them all. His faith in the high purposes of State Farm as an organization dedicated to service (was) all absorbing. And his loyalty to the men and women who were loyal to him and his ideals was legendary (Schriftgiesser, p. 229 ).

Despite his dominant personality, Mecherle had an ability to recognize his own weaknesses and to hire people to do well that which he could not do well. His executive vice president, Adlai Rust, was one such person. As Mecherles son, Ramond, once put it, Many times I have heard Dad say

that together he and Adlai Rust made a darn good team. Each one seemed to understand the other perfectly. Their different abilities somehow meshed together in a sort of happy harmony. Dad used to say, Im not a detail man. He could see the broad sweeping outlines of a plan, but Adlai could see the details and facts needed to make it work. Each complemented the other. As a team they were just unbeatable ( Schriftgiesser, p. 232).

In 1937 sixty-year old George Mecherle handed over the presidency of the company to his son Ramond and took the position of chairman of the board. He made the change partly to prepare successor management and partly because he believed the time had come for him to spend most of his time planning the companys long run strategy.

What followed were two instructive case studies showing how an ambitious plan backed by an executive willing to recognize mistakes, yet determined to achieve the plans goals, can force a company to make major organizational change.

The first case began in 1938 when the company adopted Mecherles proposal to boost the number of automobile insurance policies in force to one million by 1944. Launched with the slogan, A Million or More by 44, the campaign soon fell behind schedule and it appeared as if the goal was a bit too ambitious. But George Mecherle refused to compromise. He fought back by introducing several important organizational and operational changes. One change was the introduction of national advertising for the first time in the companys history. A second change was the development of a cooperative program with banks that made new car loans. A third, somewhat traumatic change, was the decision to replace part-time agents with full-time agents.

Those and other changes made a difference. Automobile policies in force rose from one-half million at the start of the campaign in 1938 to one million in 1944.

The second case study began in 1948 when the company set a goal of reaching one billion dollars of life insurance in force by 1954. History repeated itself as sales fell behind schedule and Mecherle, refusing to pare down the goal, turned to organizational change as a means of accelerating sales. The most important change was to introduce improved training programs for agents and to combine that training with improved incentive systems. These changes worked! The goal was achieved in 1954. But George Mecherle did not live to enjoy that accomplishment. He died in 1951.

At the time of George Mecherles death State Farm Insurance companies was the worlds largest automobile insurance company on one of the largest life insurance companies. The home office had grown from a staff of 3 people in 1922 to an organization of 2,781 employees in 1951 (including four branch offices).

This article was written by Dr. Richard Hattwick.

REFERENCES

1. Karl Schriftgiesser. THE FARMER FROM MERNA. New York: Random House, 1955.

Click for Slides related to George Mecherle

ANBHF Laureates

Our laureates and fellows exemplify the American tradition of business leadership. The ANBHF has published the biographies of our laureates and fellows.

Some are currently available online and more are added each month.

Back to Top

American National Business Hall of Fame - Contact

c/o Western Illinois University Libraries

Macomb, IL 61455

(309)298-2705